How to acquire financial literacy - simple steps for beginners

Kyiv • UNN

Only a third of Ukrainians can correctly determine the annual interest rate on a loan. The country has approved the National Strategy for the Development of Financial Literacy until 2030.

In 2026, financial literacy has become one of the tools of daily security for Ukrainians. Due to the war, economic instability, price changes, risks of income loss, and the spread of online fraud, it is important for people to understand how to plan a budget, control expenses, use banking services, avoid unnecessary debt, and protect their own funds.

How to properly plan your budget, find out what money is spent on, avoid credit traps, and accumulate a "financial safety cushion," UNN has figured out.

What is financial literacy and why is it needed

Financial literacy is a set of knowledge, skills, and habits that help a person properly manage income, expenses, savings, debts, and financial risks.

Often, mastering it begins with short and seemingly simple questions:

- how much money do I earn?

- where do I spend money?

- how much money can I save?

- do I really need a loan?

- what will happen if my income decreases tomorrow?

The main task of financial literacy is to make behavior with money conscious. A person with basic knowledge less often falls into a debt trap, reads contracts more carefully, compares the terms of banking products, does not spend all the money immediately after a salary, and gradually forms a "financial cushion."

What is the level of financial literacy among Ukrainians

The level of basic financial literacy in Ukraine remains moderate: only a third of Ukrainians can correctly determine the annual interest rate on a loan if they are given the monthly rate. At the same time, the majority of citizens tend to spend residual funds or keep them in cash or in an account, avoiding investments. This is evidenced by the results of a survey by Info Sapiens, conducted in June 2025 on the order of the NGO "Ukrainian Women's Congress" and "Oschadbank."

According to the study, Ukrainians' awareness of financial issues is mostly limited to knowledge of the exchange rate, while other topics remain less understood.

The best results are shown by people aged 30–39, while pensioners have the lowest level of financial behavior skills.

Researchers also recorded a difference between residents of large cities and rural areas: residents of large cities have a higher level of financial literacy.

A gender gap also persists: 37% of men versus about 25% of women correctly calculate the loan rate.

According to the director of Info Sapiens, Dmytro Savchuk, the level of financial literacy reflects not only basic knowledge but also practical access to financial resources.

Gender and regional inequalities are especially noticeable: women have less experience in managing funds, which creates a vicious circle of limited opportunities, and residents of rural areas and eastern regions are inferior in financial awareness to urban residents, being less well-off

The investment activity of Ukrainians also remains limited. According to the survey results, 41% of respondents are ready to invest leftover funds in deposits or other financial instruments. At the same time, if they imagine receiving a significant amount, the share of those who would consider investments increases to 61%.

The most inclined to invest are residents of the West and large cities. The least are residents of villages and eastern regions. At the same time, women more often prefer investments in real estate, and men in business development.

The study also showed that only half of Ukrainians would turn to a bank in case of an urgent need for a loan. At the same time, every eleventh person is ready to borrow money from non-banking organizations or strangers, which may increase the risk of falling into debt dependence.

Among the main reasons why they avoid bank lending, the surveyed Ukrainians cited distrust, complexity of conditions, high interest rates, and bureaucracy.

The level of knowledge about the filling of local budgets also remains insufficient. 69% of respondents understand that the main revenues are formed by local taxes and fees, however, among young people, rural residents, and residents of the East, confusion on this issue is more often observed.

At the same time, the demand for financial education in Ukraine is high. Interest in free courses was expressed by 53% of women and 44% of men.

The most popular topics for learning were starting one's own business, grant programs, savings and investments, as well as the community budget.

The form of learning depends on the region: in general, Ukrainians more often choose the online format, however, residents of the South and East more often prefer offline classes.

Separately, the study revealed gender differences in financial relations within households. In particular, 37% of women and 27% of men sometimes ask their partner for money. More than a quarter of respondents find such requests offensive.

These data show that the level of financial literacy remains limited, but at the same time there is a clear demand for change, especially from women and young people. This is an opportunity for the state, business, and public initiatives to develop educational programs adapted to the needs of different population groups

Basics of financial literacy that everyone should know

The first basic principle is that income and expenses need to be known precisely. Many people are sure that they "spend almost nothing" until they see the monthly amount on coffee, deliveries, taxis, or small purchases. This is where expense tracking comes in handy, which shows the cash flow for the month. You can record your income and expenses in a regular notebook, special notebooks that can be purchased in bookstores, or use thematic mobile applications.

The second principle is that the budget needs to be planned for:

- a day;

- a week;

- a month;

- a year.

The simplest option is to divide expenses into mandatory, variable, and optional.

Mandatory expenses include housing, utilities, food, communication, medicine, loans.

Variable expenses include transport, clothing, household goods.

Optional expenses include entertainment, impulsive purchases, and subscriptions that no one has used for a long time.

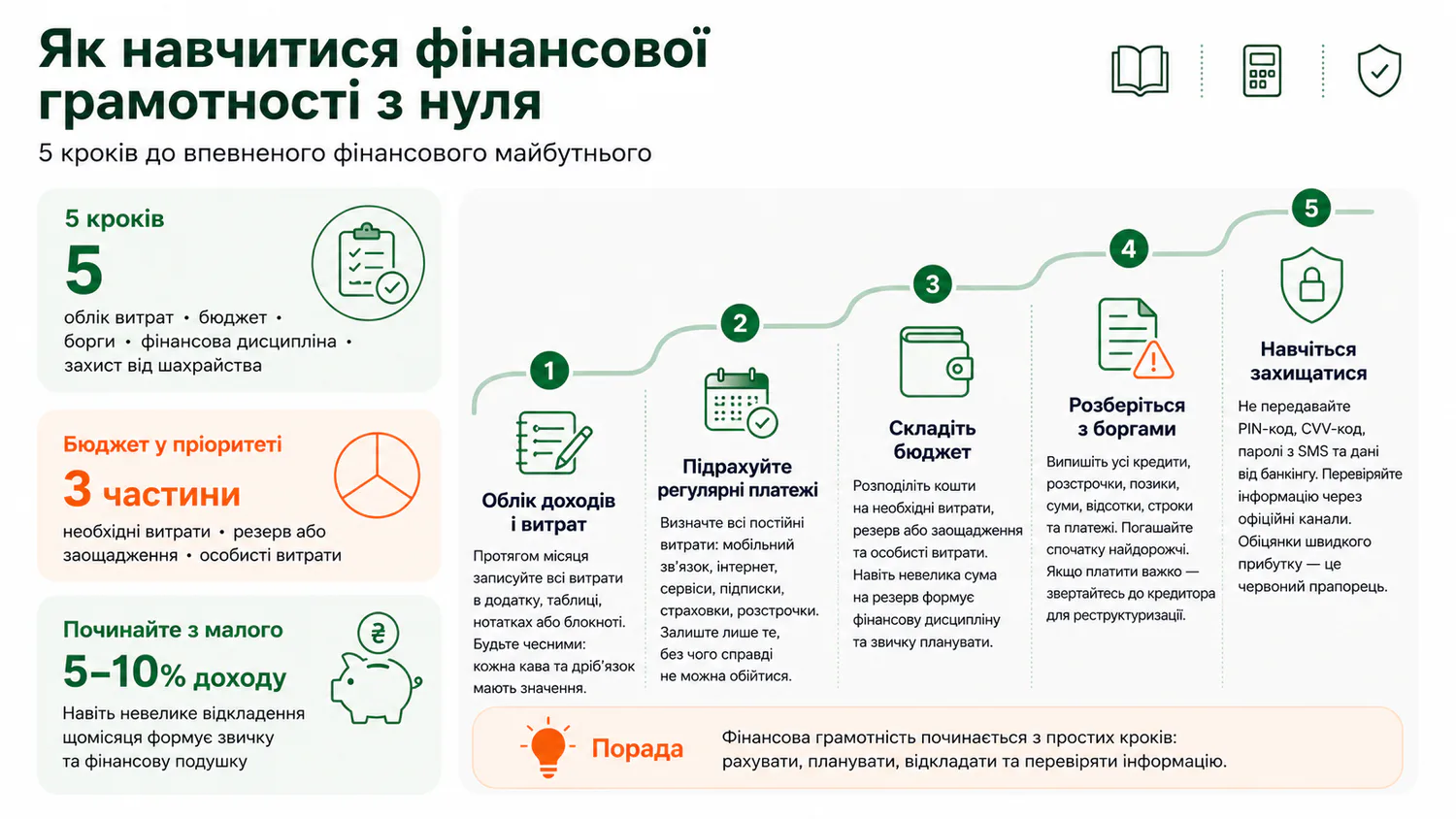

The third principle is based on the fact that even with minimal income, you need to try to create a "financial safety cushion." This is a reserve in case of job loss, illness, moving, equipment repair, or other unforeseen expenses.

It is optimal to gradually accumulate an amount that covers three to six months of basic expenses. You can start small: even 5–10% of income every month already forms a useful habit.

The fourth principle is a cautious attitude towards debts.

Problems begin exactly at the moment when a person takes a loan from an MFO, uses the credit limit on a bank card, or takes out a cash loan from a bank and does not understand their real cost, does not know about fines, fees, terms, and consequences of delay.

That is why, before signing any loan agreement, it is worth looking at both the monthly payment and the total cost of the loan.

The fifth principle is protection against fraud. You cannot give strangers your PIN code, CVV code, SMS passwords, or banking login details. Banks do not ask for this data by phone or in messengers. If a message promises "compensation," "aid," or "winnings," it is better to check the information through official channels.

How to learn financial literacy from scratch

You should start not with investments or trendy advice on social networks, but with organizing your own budget.

The first step is to record all expenses for one month.

The second step is to calculate regular payments. Often, it is they that imperceptibly "eat up" part of the income. These include:

- mobile communication;

- internet;

- subscriptions;

- insurance;

- installment plans.

After that, it is worth asking yourself what you really cannot do without, and what you can give up and save on.

The third step is to draw up a simple budget for the next month. It should have three parts: necessary expenses, reserve or savings, personal expenses. Even if the income is small, it is important to include at least a minimum amount for the reserve. Financial discipline is formed not when there is a lot of money, but when the habit of planning appears.

The fourth step is to deal with debts. You need to write down all loans, installments, borrowings, the amount of debt, interest, mandatory payments, and deadlines. The most expensive loans should be repaid first. If payments have become unbearable, it is better to contact the creditor and discuss restructuring.

The fifth step is to learn to distinguish financial information from financial noise. Advice from the internet needs to be checked: who gives it, whether that person has a professional reputation, whether they are selling a "unique course" or "guaranteed earnings." In finance, promises of quick profit are usually a warning sign.

Rules of financial literacy that always work

The first rule is to spend less than you earn per month. If expenses consistently exceed income, no microloan or credit limit from a bank will solve the problem.

The second rule is to "pay" yourself first. This means setting aside part of your income immediately after receiving the money. An automatic transfer to a separate account helps make such saving a habit.

The third rule is not to take a loan for something that quickly loses value or is not necessary. Equipment, treatment, or education can be justified expenses if a person understands their capabilities. But a loan for impulsive purchases, vacations, or status items often only postpones the problem to the future.

The fourth rule is to have a financial goal. It is better to define a specific goal: reserve, education, housing, renovation, moving, pension savings. The goal should have a clear cost and an approximate accumulation period.

The fifth rule is to regularly review financial decisions. Once every few months, it is worth checking bank tariffs, deposit terms, insurance, communication costs, subscriptions, and loans.

Financial literacy tips for Ukrainians of different ages

For children, it is better to explain financial literacy through play. In addition, you can and should:

- give the child pocket money;

- allow them to make small purchases;

- help them save for a desired item;

- talk about the difference between "want" and "need."

For teenagers, it is worth telling about how:

- bank cards work;

- what online payments are;

- what fraudulent schemes exist and how not to become their

victim;

- why you don't always need to buy what is advertised;

- what is the danger of loans and installment plans.

A separate topic is a critical attitude towards "easy money" on the internet. Teenagers need to be explained that behind offers to easily and quickly earn big money are usually either people involved in drug trafficking, or Russian special services that use young men and women for sabotage.

For young adults, it is important to learn how to plan their first stable income. It is during this period that habits are formed that then either help or hinder for years. It is worth avoiding unnecessary debts, creating a reserve, investing in education and professional skills.

For middle-aged people, it is worth focusing on the balance between current expenses, family support, insurance, large purchases, and long-term savings. If there are loans or financial obligations to relatives, the budget should take into account not only desires but also risks.

For older people, it is especially important to take care of the safety of funds, avoid dubious investments, check information about social payments, not give card details to strangers, and have a clear plan of regular expenses.

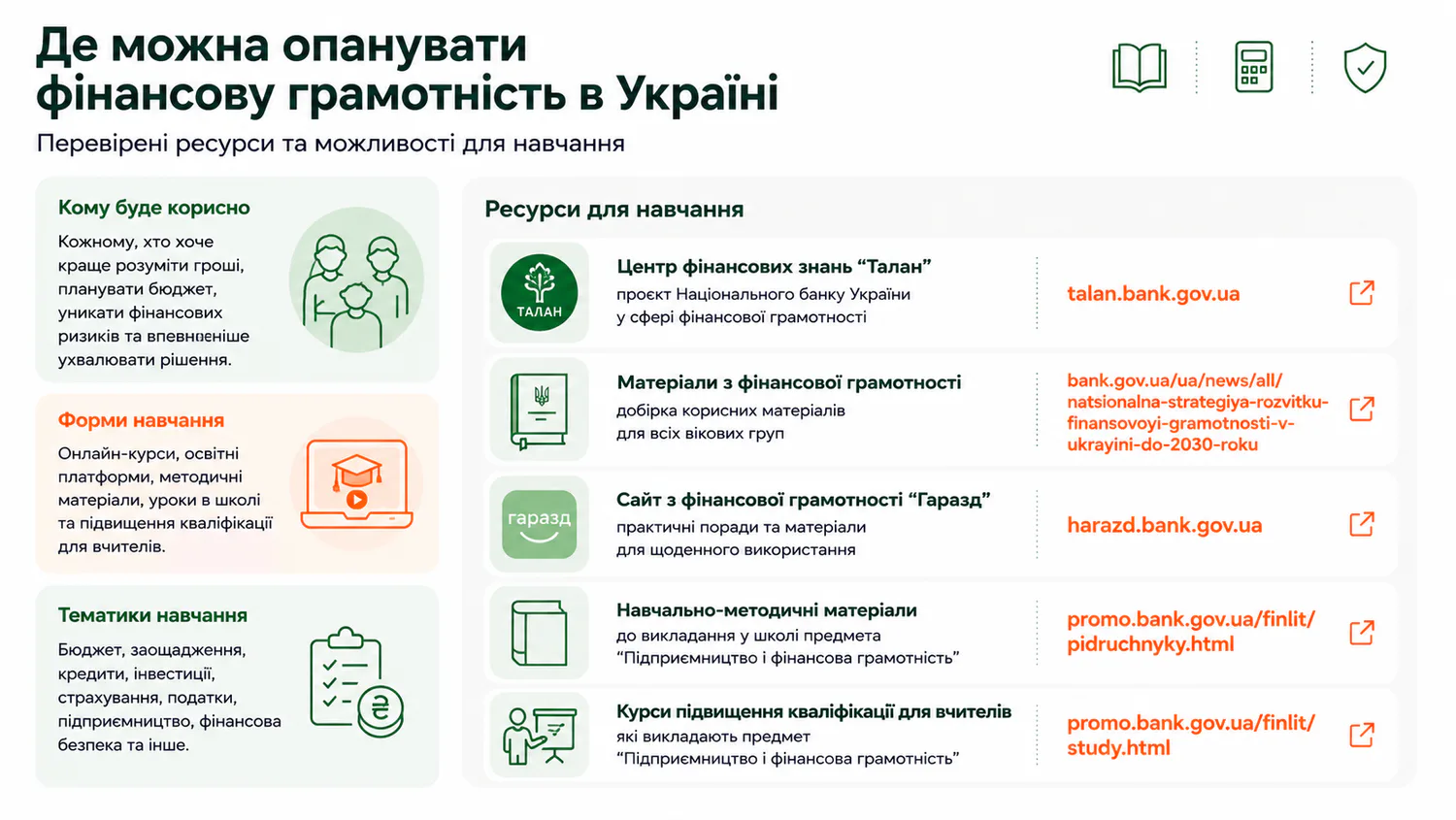

Where you can master financial literacy in Ukraine

Note that Ukraine has approved the National Strategy for the Development of Financial Literacy until 2030. Its goal is to help Ukrainians better understand how money, financial services, savings, loans, investments, and other financial instruments work.

The document should help people make financial decisions more confidently, better plan their own budget, use banking and other financial services more responsibly, and also avoid thoughtless expenses and financial risks.

The strategy was developed by several state institutions: the National Bank of Ukraine, the Ministry of Education and Science, the Deposit Guarantee Fund, the National Securities and Stock Market Commission, the Ministry of Economy, the Ministry of Digital Transformation, and the Office for Entrepreneurship and Export Development.

One of the main directions of the Strategy is to create a comprehensive system of financial education in Ukraine. This means that various state bodies, educational institutions, financial organizations, and other participants should work in a coordinated manner, rather than each on their own, as is often the case in state initiatives.

Previously, financial literacy programs were mainly aimed at children and youth, as they had the lowest level of financial knowledge. Now, attention is also planned to be given to adults, entrepreneurs, veterans, internally displaced persons, and the elderly.

Work on the Strategy began back in June 2021. After the start of Russia's full-scale aggression, it was temporarily suspended in March 2022, and resumed in September 2023.

During the preparation of the document, Ukraine relied on international experience, in particular the recommendations of the Organisation for Economic Co-operation and Development and the approaches of the International Network on Financial Education, of which Ukraine is a member.

The Strategy was approved by the relevant decisions of the developer institutions. At the National Bank, it was approved by the decision of the NBU Board on April 12, 2024, and in September 2025, amendments were made to the document.

In this regard, several projects are being implemented in our country, and several tools for financial education of the population have already been launched. Currently, Ukrainians can use the following resources:

- The "Talan" Financial Knowledge Center (a project of the National

Bank of Ukraine in the field of financial literacy): https://talan.bank.gov.ua/;

- materials of the National Strategy for the Development of Financial

Literacy until 2030: https://bank.gov.ua/ua/news/all/natsionalna-strategiya-rozvitku-finansovoyi-gramotnosti-v-ukrayini-do-2030-roku;

- the financial literacy website "Harazd": https://harazd.bank.gov.ua/;

- educational and methodological materials for teaching the subject

"Entrepreneurship and Financial Literacy" at school: https://promo.bank.gov.ua/finlit/pidruchnyky.html;

- professional development courses for teachers who

teach the subject "Entrepreneurship and Financial Literacy": https://promo.bank.gov.ua/finlit/study.html.

Reminder

Earlier we wrote that in high school, students are planned to be taught financial literacy.